3. Recording of transaction-I | Preparation of Accounting Vouchers Accounts class 11

3. Recording of transaction-I | Preparation of Accounting Vouchers Accounts class 11

Preparation of Accounting Vouchers

Preparation of Accounting Vouchers :

Preparation of Accounting Vouchers :

Accounting vouchers may be classified as

(i) Cash vouchers,

(ii) Debit vouchers,

(iii) Credit vouchers,

(iv) Journal vouchers, etc.

There is no set format of accounting vouchers.

The Specimen of Transaction Voucher

Transaction Voucher:

A transaction with one debit and one credit is a simple transaction and the accounting vouchers prepared for such transaction is known as Transaction Voucher.

There are Three types of Vouchers:

(i) Compound Voucher : Voucher which records a transaction that entails multiple debits/credits and one credit/debit is called compound voucher.

Compound voucher may be:

(a) Debit Voucher or

The Specimen of Debit Voucher:

(b) Credit Voucher

The Specimen of Credit Voucher :

(ii) Complex Voucher/Journal Voucher : Transactions with multiple debits and multiple credits are called complex transactions and the accounting voucher prepared for such transaction is known as Complex Voucher/ Journal Voucher.

The design of the accounting vouchers depends upon the nature, requirement and convenience of the business.

To distinguish various vouchers,

⇒ different colour papers and

⇒ different fonts of printing are used.

A accounting voucher must contain the following essential elements :

• It is written on a good quality paper;

• Name of the firm must be printed on the top;

• Date of transaction is filled up against the date and not the date of recording of transaction is to be mentioned;

• The number of the voucher is to be in a serial order;

• Name of the account to be debited or credited is mentioned;

• Debit and credit amount is to be written in figures against the amount;

• Description of the transaction is to be given account wise;

• The person who prepares the voucher must mention his name along with signature; and

• The name and signature of the authorised person are mentioned on the voucher.

Accounting Equation

Accounting Equation :

Total Assets = Total Liabilities

Or

Total Assets = Internal Liabilities + External Liabilities

Or

Total Assets = Capital + Liabilities

Accounting equation signifies that the assets of a business are always equal to the total of its liabilities and capital (owner’s equity).

A = L + C

Where,

A = Assets

L = Liabilities

C = Capital

Now,

(i) A – L = C

(ii) A – C = L

The accounting equation depicts the fundamental relationship among

the components of the balance sheet, it is also called the Balance Sheet Equation.

⇒ The balance sheet is a statement of assets, liabilities and capital.

⇒ The claim of the proprietors is called capital and that of the outsides is known as liabilities.

⇒ Each element of the equation is the part of balance sheet, which states the financial position of the business on a particular date.

⇒ When we analyse the transactions, we actually try to know that how balance sheet of a business entity gets affected.

⇒ Asset side of the balance sheet is the list of assets, which the business entity owns.

⇒ The liabilities side of the balance sheet is the list of owner’s claims and outsider’s claims, i.e., what the business entity owes.

⇒ The equality of the assets side and the liabilities side of the balance sheet is an undeniable fact and this justifies the name of accounting equation as balance sheet equation also.

Classification of Transactions:

Following are the nine basic transactions:

(1) Increase in assets with corresponding increase in capital.

(2) Increase in assets with corresponding increase in liabilities.

(3) Decrease in assets with corresponding decrease in capital.

(4) Decrease in assets with corresponding decrease in liabilities.

(5) Increase and decrease in assets.

(6) Increase and decrease in liabilities

(7) Increase and decrease in capital

(8) Increase in liabilities and decrease in capital

(9) Increase in capital and decrease in liabilities.

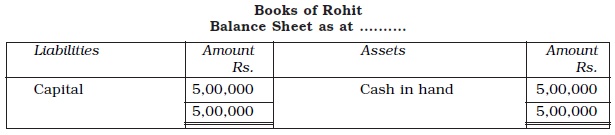

Example: Rohit started business with a capital of Rs. 5,00,000.

Solution:

From the accounting point of view we see:

(i) The resources of this business entity is in the form of cash, i.e., Rs. 5,00,000.

(ii) Sources of this business entity is the contribution by Rohit (Proprietor) Rs. 5,00,000 as Capital .

"In the above balance sheet, the total assets are equal to the liabilities of the business."

Example 1.

1. Opened a bank account in State Bank of India with an amount of

Rs. 4,80,000.

Analysis of transaction: This transaction increases the cash in hand

(assets) and decreases cash (asset) by Rs. 4,80,000.

2. Bought furniture for Rs. 60,000 and cheque was issued on the same day.

Analysis of transaction: This transaction increases furniture (assets) and

decreases bank (assets) by Rs. 60,000.

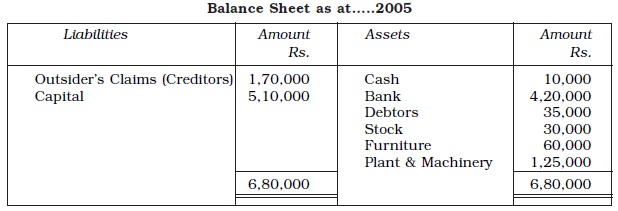

3. Bought plant and machinery for the business for Rs. 1,25,000 and an advance of Rs. 10,000 in cash is paid to M/s Ramjee Lal.

Analysis of transaction: This transaction increases plant and machinery

(assets) by Rs. 1,25,000, decreases cash by Rs. 10,000 and increases

liabilities (M/s Ramjee lal as creditor)by Rs. 1,15,000.

4. Goods purchased from M/s Sumit Traders for Rs. 55,000.

Analysis of transaction: This transaction increases goods (assets) and

increases liabilities (M/s Sumit Traders as creditors) by Rs. 55,000.

5. Goods costing Rs. 25,000 sold to Rajani Enterprises for Rs. 35,000.

Analysis of transaction: This transaction decreases stock of goods (assets) by Rs. 25,000 and increases assets (Rajani Enterprises as debtors Rs. 35,000) and capital (with the profit of Rs. 10,000)

Solution:

In terms of accounting equation

A = L + C

Rs. 6,80,000 = Rs. 1,70,000 + Rs. 5,10,000

Rules of Debit and Credit

Rules of Debit and Credit

All accounts are divided into five categories for the purposes of recording the transactions:

(a) Asset

(b) Liability

(c) Capital

(d) Expenses/Losses, and

(e) Revenues/Gains.

Two fundamental rules are followed to record the changes in these accounts:

(1) For recording changes in Assets/Expenses (Losses):

(i) “Increase in asset is debited, and decrease in asset is credited.”

(ii) “Increase in expenses/losses is debited, and decrease in expenses/

losses is credited.”

(2) For recording changes in Liabilities and Capital/Revenues (Gains):

(i) “Increase in liabilities is credited and decrease in liabilities is debited.”

(ii) “Increase in capital is credited and decrease in capital is debited.”

(iii) “Increase in revenue/gain is credited and decrease in revenue/gain is debited.”

Books of Original Entry

Journal : The book in which the transaction is recorded for the first time is called journal or book of original entry.

(i) Journalising : The process of recording transactions in journal is called journalising.

(ii) Posting : The process of transferring journal entry to individual accounts is called posting.

The book of original entry: This sequence causes the journal to be called the Book of Original Entry and the ledger account as the Principal Book of entry.

Entry process is like this:

Entry into the Journal (Journalising)

⇓

Transfer to the indivisual accounts (Posting to Leader)

(E.g: cash account, sale account, purchage account, bank account)

⇓

The journal is subdivided into a number of books of original entry as follows:

(a) Journal Proper

(b) Cash book

(c) Other day books:

(i) Purchases (journal) book

(ii) Sales (journal) book

(iii) Purchase Returns (journal) book

(iv) Sale Returns (journal) book

(v) Bills Receivable (journal) book

(vi) Bills Payable (journal) book

Journal and Ledger

JOURNAL AND LEDGER

JOURNAL - Journal is a book of prime entry or book of original entry in which transactions are first recorded in chronological order.

FEATURES OF A JOURNAL -

- It shows complete record of transactions.

- It is a book of original entry in which transactions are first recorded.

- Day to day transactions are recorded in a journal in chronological order.

- It records both aspects of a transaction i,e. debit and credit.

ADVANTAGES OF JOURNAL -

- It helps to provide accounting data in chronological order.

- It reduces possibility of errors by recording transactions both sides debit as well as credit.

- It provides explanations of transactions along with recording in journal for better understanding of transactions.

- It hepls in ledger posting of transactions.

- It ensures arthmetical accuracy.

- Classification of all transactions become easier.

LIMITATIONS OF JOURNAL -

- It is unsuitable for large volume of transactions.

- It is not a simple system of recording of transactions.

- It is not a substitute of ledger.

- It is time consuming process.

- It does not facilitate internal control, because in journa,l transactions are recorded in chronological order.

FORMAT OF JOURNAL -

|

Date |

Particulars |

L.F. |

Dr.(amount) |

Cr.(amount) |

|

|

|

|

|

|

Journal is divided into 5 columns. These are as follows -

1. Date

2. Particulars

3. Ledger Folio

4. Debit Amount

5. Credit Amount

Example - Mr. A started business and introduced capital of rs. 5,00,000.

the transaction is recorded by passing following journnal entry :

|

Date |

Particulars |

L.F. |

Dr(amount) |

Cr(amount) |

|

|

Bank A/c Dr... To Capital A/c |

|

5,00,000

|

5,00,000 |

LEDGER -

- Means a book which contains, in a summerisedand and classified record of all transactions.

- Ledger is called principal book of account.

- Ledger is called book of final entry.

FEATURES OF LEDGER -

- It is prepred from journal.

- Trial balance and final accounts are prepared from ledger accounts.

- Ledger accounts shows current balances of all accounts.

- Ledger is a master record of all transactions

- It holds relevent informations at one place relating to a particular account.

UTILITY OF LEDGER -

- ledger helps to prepare a separate account for each income and expense.

- It provides complete information about a particular account.

- It helps in prepration of trial balance.

- It also helps in prepration of final accounts. I,e. trading A/c, P&L A/c and balance sheet.

FORMAT OF LEDGER ACCOUNT -

Dr. Cr.

|

Date |

Particulars |

J.F. |

Amount(Rs.) |

Date |

Particulars |

J.F. |

Amount(Rs.) |

|

|

|

|

|

|

|

|

|

Share this Notes to your friends:

Accounts Chapter List

Select Class for NCERT Books Solutions

NCERT Solutions

sponder's Ads